📊Are Shorter Term Fixed Mortgages A Better Choice?🔮

There are many decisions to make when arranging a new mortgage. Whether to go with a fixed or variable, amortization period, payment frequency, and term length.

Prior to mortgage rule changes that came into effect on November 30, 2016, short term mortgages usually came with lower rates than the 5 year options. The shorter the term, the lower the rate. Times have changed, and there hasn’t been much interest in shorter term mortgages ever since.

Fast forward to today, and shorter-term mortgages are still priced higher in many cases, but they are now making a comeback in a very big way.

Contrary to popular belief, the most important part of your mortgage is not the rate.

It’s not even the savings over the term.

Sure, these are all important, but what’s most important is how much you will save over the life of your mortgage.

You can maximize your overall savings by having the right strategy, and sometimes choosing a product with a higher rate with a shorter commitment can lead to more savings down the road.

Locking In When Fixed Rates Are The Highest since 2008

Anyone choosing a 5 year fixed mortgage rate today would be locking in at their highest point in fourteen years. That doesn’t necessarily make it the wrong choice. It comes down to what you feel most comfortable with and what is right for one person might not be right for the next.

The alternatives are a 5 year variable or a shorter term fixed rate (variable rate mortgages are seldom offered in terms less than 5 years).

Even with more increases to prime rate expected, variable rates still have a chance at outperforming fixed rates. You can read about this in detail in my recent blog: Should Variable Rates Be Avoided.

But if you’re looking for a happy medium, then a shorter-term fixed rate is a viable option.

Let’s first look at what is being forecasted moving forward before coming to a conclusion.

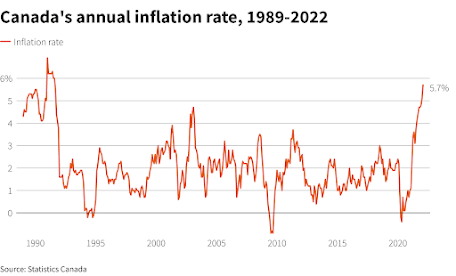

Is inflation Now Decreasing?

We all know we have an inflation problem on our hands, which is what the Bank of Canada is trying to bring under control by increasing rates. Inflation dropped in July and then again in August. In fact, analysts were expecting inflation to drop to 7.3% in August, but it dropped even further to 7%. Hard to imagine that we would see a time where 7% inflation is a good sign, but it’s not the number that is the good news. It’s the fact that it dropped, and that it dropped further than what was expected.

The question is, will inflation drop again when they release the December report next month?

Let’s hope.

The recent drop could be a sign that the Bank of Canada rate increases are now starting to work as intended. We’ll see.

The rapidly increasing rates have scared a lot of people, particularly those in variable rate mortgages, or for those who have mortgages that are coming up for renewal.

The biggest reason why inflation is out of control is because of the limited supply chain. The Bank of Canada knows that increasing rate is going to do nothing to improve the supply. They have no control over that. But their intention is to weaken the economy, which would bring demand down in line with the current supply. They have been trying to avoid using the word ‘recession’ as they don’t want to talk themselves into it becoming a reality. But by intentionally trying to push demand down, this is exactly what they are pushing for.

The Road To Mortgage Rate Cuts

The Bank of Canada will eventually reach their inflation goal of 2.00% and the supply will eventually return.

By this time, our economy will be so badly damaged that the Bank of Canada will need to make it their number one priority. They will need to stimulate the demand by lowering their rate. The worse the economy, the more aggressive they will need to get with their rate cuts.

When the Bank of Canada starts to cut their rate, or even when there is a hint that a rate cut is on the way, bond yields can then be expected to fall. This will put downward pressure on fixed rates which will then start to drop.

The more aggressive the Bank of Canada was with their rate increases, the more aggressive they may have to be with their cuts. It’s possible that we could see both prime rate and fixed rates start to plummet in 2024 as many are expecting.

2 Year Fixed vs. 5 year Fixed

This is why a shorter term fixed rate mortgage can be a great choice, even if the rate is higher than the 5 year option. If you chose a 5 year fixed product today, it would not come up for renewal until late 2027. It’s anyone’s guess as to where rates will be at that time.

A 2 year fixed rate today would come up for renewal in late 2024… which could be perfect timing to take advantage the forecasted rate cuts if they come through as currently predicted.

The lowest 2 year fixed is currently 4.84%* with the lowest 5 year fixed at 4.64%* The difference between the two options on a $500,000 mortgage works out to roughly $2,009 by the end of 2 years.

Let’s say the 5 year fixed rate at the end of the 2 year term is 2.99%. If you chose the 5 year option at 4.64%, you’d still have three years to go at the higher rate. But if you chose the 2 year option, you would save $23,289 in the remaining 3 years. Subtract the additional $2,009 that it cost you for the 2 year term at the beginning, and you’re ahead by roughly $21,000 at the end of five years.

This is of course a hypothetical situation which I’m using as an example. No one can say where the rates will be in 3 years, but based on the current economic forecasts, it could very well be reality.

Conclusion

There is still a lot of uncertainty moving forward, and a shorter-term fixed rate can be a great choice over the more volatile variable rate options.

Eventually rates will drop. It’s just a matter of when. It all comes down to how quickly the Bank of Canada can get inflation under control. If current forecasts hold, then we can expect rates to be lower within the next couple of years. Time will tell and anything can happen.