⚠️Consolidating Debt Into Your Mortgage♻️

High levels of debt can significantly eat into monthly cash flow which can take a toll on many households. Particularly those who are living paycheque to paycheque.

Rising inflation is not making it any easier.

There may be ways to utilize the equity in your home to significantly reduce your debt payments to increase your cash flow, which can give you a bit more breathing room financially.

The average non-mortgage debt per Canadian consumer rose to $21,183 in the third quarter of 2022 according to Equifax. Rising mortgage rates has not made it any easier for people, particularly for those in variable rate mortgages and those with mortgages coming up for renewal. Inflation has been driving up the cost of just about everything, further fueling consumer debt which is not making it any easier for many people.

Types of Consumer Debt

There are many different types of consumer debt, all with varying interest rates, terms, payments, etc.:

Mortgages

HELOCs (Home Equity Line of Credit)

Car loans

Personal loans

Personal lines of credit

Student loans

Mortgages are often considered as ‘good debt’ as they are what makes homeownership possible. Without them, everyone would just be throwing their money away on rent. But other debt can create misery if it gets out of control and can even lead to broken marriages. This is why cash flow is so important as it can significantly reduce or even eliminate financial stress.

Increasing Your Cash Flow

It’s not always about moving debt to a lower interest rate. For many struggling households, it’s about improving cash flow to provide a release from the burden of higher monthly payments.

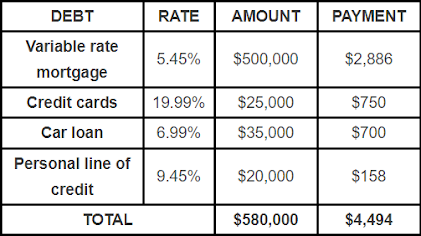

We’ll create a fictitious couple to illustrate and all too common situation. Jim Bob and Michelle live in a modest home with their 19 kids. (Okay, maybe 19 is a bit much, but hope that at least made you smile). They have an annual household income of $120,000 before taxes and have a variable rate mortgage where the payments change with prime rate. When they bought their home two years ago, their rate was only 1.45% which was easily manageable as their monthly payment was only $1,815. Just like everyone else, they never thought that the Bank of Canada would have increased their rate by 4.00% in 2022, bringing their rate up to 5.45% and increasing their monthly payment to $2,885. Over $1,000 more than what it was originally.

Their increasing mortgage payment along with overall inflation has resulted in rising debt which is starting to get out of control considering their modest income:

Once they have paid their property taxes, groceries, utilities, and other general expenses, they have virtually no money left over at the end of the month.

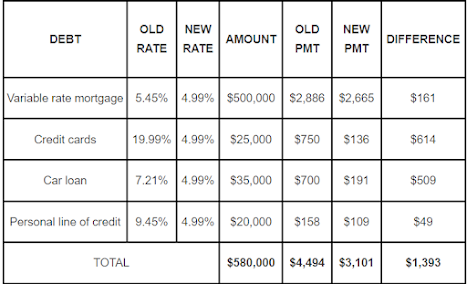

If we were to refinance the above debt into a new fixed rate mortgage at 4.99% then the new monthly payment structure would look like this if we broke it down piece by piece:

Everything would of course be lumped into a single mortgage and payment, but I’ve broken it down so you can see how each component is affected individually. By refinancing their mortgage to consolidate all their debt, they are increasing their monthly cash flow by $1,393 per month and will no longer need to worry about living paycheque to paycheque.

But isn’t this just stretching out the debt over a longer period?

Yes, it is, but this is more about increasing cash flow and relieving financial stress than maximizing savings long term. If you stick with the new payment structure for the next 30 years, then yes, you’re now taking 30 years to pay off your car (for example).

But there is an alternative strategy.

If you can comfortably do so, then I suggest using your prepayment privileges to increase your payment to match the debt you are consolidating. In the above example, the $700 car loan was reduced by $509. You can then increase your mortgage payment by $509 resulting in the exact same car payment you were previously making. 100% of the payment increase will go straight to your principal. The car loan portion of the mortgage would then be paid off in less time than the original loan given the lower rate.

Conclusion

This strategy is based on refinancing your mortgage, but there are other options for accessing your home’s equity without having to break your mortgage.

There are many things to consider before we can determine if consolidating your debt into your mortgage is right for you. Break penalties, refinancing costs, rates, etc. Different people have different financial goals.

For some people, maximizing cash flow is their number one priority.

For others, it will be paying the least amount of interest over time. Sure, you can say you want both, but you can’t have your cake and eat it too. Going off track here for a second, I’ve always found that a funny line… why would someone have cake and not want to eat it? Makes no sense. I digress.

Consolidating debt into a mortgage can be the difference between struggling financially or living comfortably without having to worry about how you’re going to make your next mortgage payment. Every situation can be a bit different, so it’s best to reach out to us directly so we can analyze your specific situation for you in detail.